The Details Of Home Mortgages

Created by-Marker Kent

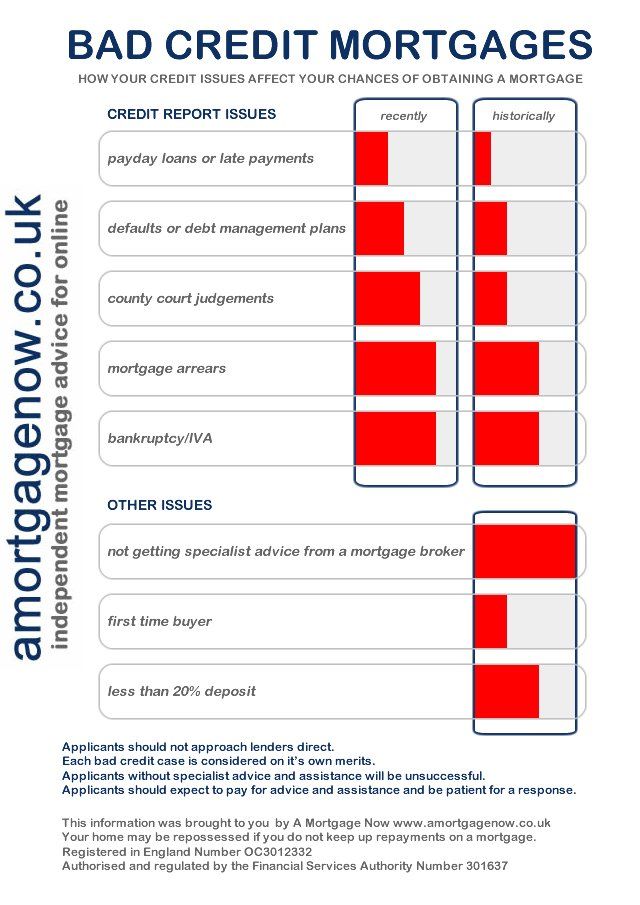

How is mortgage defined? A home loan helps to get you into a new home, and it's secured by the home you buy itself. If you are unable to pay for it, the bank will foreclose on it. This is a big responsibility, but the tips below can help you through it.

When you get a quote for a home mortgage, make sure that the paperwork does not mention anything about PMI insurance. Sometimes a mortgage requires that you get PMI insurance in order to get a lower rate. However, the cost of the insurance can offset the break you get in the rate. So look over this carefully.

Beware of low interest rate loans that have a balloon payment at the end. These loans generally have lower interest rates and payments; however, a large amount is due at the end of the loan. This loan may seem like a great idea; however, most people cannot afford the balloon payment and default on their loans.

If your house is worth less than what you owe and you've been unsuccessful in refinancing it, try again. New programs (HARP) are in place to help homeowners out in this exact situation, no matter how imbalanced their mortgage and home value seems to be. Discuss your refinancing options with your lender. If the lender will not work with you, make sure you find someone else who will.

Never take out a new loan or use your credit cards while waiting for your home mortgage to be approved. This simple mistake has the potential of keeping you from getting your home loan approved. Make sacrifices, if need be, to avoid charging anything to your credit cards. Also, ensure each payment is received before the due date.

Do not take out a mortgage loan for more than you can comfortably afford to pay back. Sometimes lenders offer borrowers a lot more money than they need and it can be quite tempting since it would help you purchase a bigger house. Decline their offer because it will lead you into a debt pit you cannot get out of.

Use local lenders. If you are using a mortgage broker, it is common to get quotes from lenders who are out of state. Estimates given by brokers who are not local may not be aware of costs that local lenders know about because they are familiar with local laws. This can lead to incorrect estimates.

Be sure to keep all payments current when you are in the process of getting a mortgage loan. If you are in the middle of the loan approval process and there is some indication that you have been delinquent with any payments, it may affect your loan status in a negative way.

Speak with many lenders before selecting the one you want to borrow from. Ask family and friends about their reputation, their rates and about any of their hidden fees they have in their contracts. When you have all the details. you can select the best one.

If you have filed for bankruptcy, you may have to wait two or three years before you qualify for a mortgage loan. However, simply click the next document may end up paying higher interest rates. The best way to save money when buying a home after a bankruptcy is to have a large down payment.

Many computers have built in programs that will calculate payments and interest for a loan. Use the program to determine how much total interest your mortgage rate will cost, and also compare the cost for loans with different terms. You may choose a shorter term loan when you realize how much interest you could save.

Save up enough so you can make a substantial down payment on your new home. Although linked web site may sound strange to pay more than the minimum required amount for the down payment, it is a financially responsible decision. You are paying a lot more than the asking price for the home with a mortgage, so any amount that you pay ahead of time reduces the total cost.

After applying for a home loan, ask your lender for a copy of the good faith estimate. This contains vital information about the costs associated with your home loan. Information includes the approximate cost of appraisals, commissions and surveys along with any points that are included in the loan agreement.

Ensure that your mortgage does not have any prepayment penalties associated with it. A prepayment penalty is a charge that is incurred when you pay off a mortgage early. By avoiding these fees, you can save yourself thousands. Most of today's loans do not have prepayment penalties; however, some still do exist.

Before you begin home mortgage shopping, be prepared. Get all of your debts paid down and set some savings aside. You may benefit by seeking out credit at a lower interest rate to consolidate smaller debts. Having your financial house in order will give you some leverage to get the best rates and terms.

Know how much you will be required to pay in fees prior to signing any agreement for the mortgage. Ask the company to itemize each closing cost, including commissions and other charges. Certain things are negotiable with sellers and lenders alike.

Do not fail to have inspections. Inspections can be expensive but repairs can dwarf any savings you get by not having the inspection. Most mortgage lenders require inspections as part of the lending process. If you skip them it could hold up your loan, or even cause it to fall through.

If you want to negotiate, check with other lenders in your area. Many people are surprised to learn that some banks, and especially those that are not Internet-only banks, offer rates that beat those of larger banks. Talk about this with your lending officer to find the best deal.

With the advice that has been given to you, you are now equipped to enter the mortgage market and begin deciding which route you want to take. It's important that you understand all of your options, and you want to feel in control and not thrown into a mortgage by a lender that doesn't fit your needs. Instead, go forth and get the right mortgage!